https://fortune.com/2025/04/20/bond-market-chaos-hedge-funds-world-shadow-banks-regulation/

// Fortune article is behind a paywall.

I saw this headline the other day that some folks shared on social media: “Hedge funds are the new ‘shadow banks’—and some are worried they pose a systemic threat to financial stability.” In my head, I found the headline utterly stupid, primarily because anything outside traditional banking is considered a shadow bank, or shadowy. Nonbanks are outside the realm of heavy-duty regulation, and thus are considered a shadow bank that dwells in the realm of the shadow banking system. The shadow name simply implies that historically, nonbank entities were usually not under the same government or regulatory oversight as the big traditional banks.

Hedge funds, in particular, are not “new” shadow banks, as the headline suggested, and their growing concern as systemically destabilizing was foreseen long ago, since Long Term Capital Management in 1997. There have been Congressional hearings on hedge funds since 2008 (probably before then), and its growing concern about them being a systemic risk. Investment banking, like hedge funds, has steadily grown since the 1980s. Gone are hedge funds’ humble origins. Alfred Winslow Jones, a sociologist and financial journalist, is credited with establishing the first hedge fund in 1949. Warren Buffett claimed the idea of a hedge fund could be credited long before it was officially granted to Alfred Winslow Jones, to the time of the author of The Intelligent Investor, Benjamin Graham.

Since studying the financial system for some time now, I am in agreement that hedge funds are a danger to the financial system.

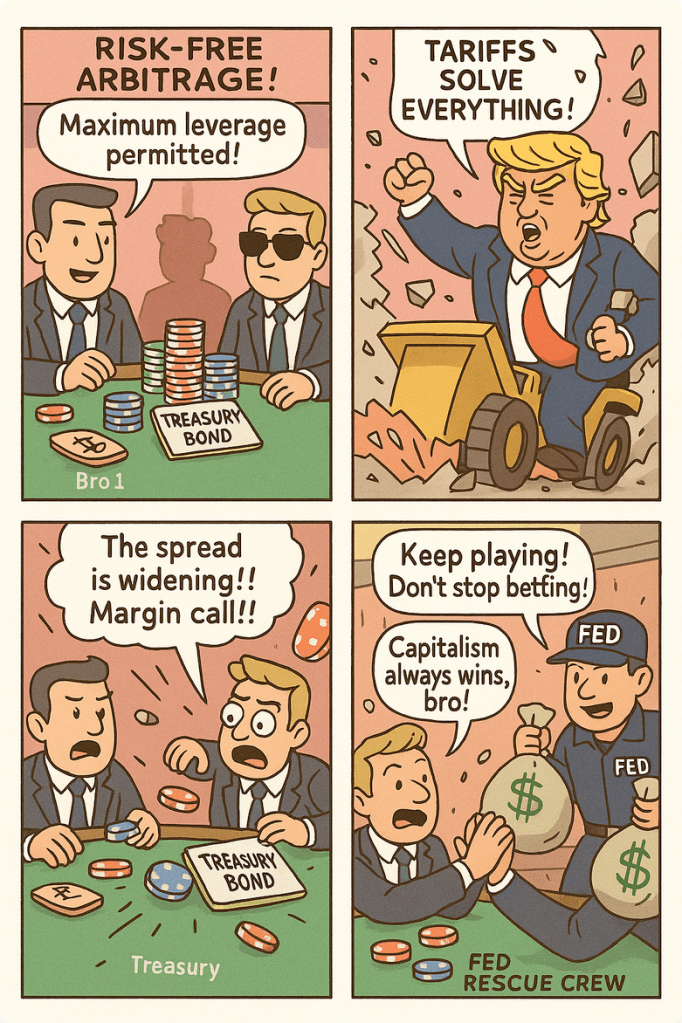

When it seemed that much of the world was mocking President Donald Trump for imposing ridiculous tariffs, from the moment he pulled out the reciprocal tariff chart for the world to see, and thus initiating a trade war, some people quietly ignored or did not notice the ripple effects it revealed about the fragility of capital markets. In other words, the real reason for Donald Trump’s 90-day pause was specifically due to concerns of what appeared to be a repeat of a 2008-like financial crisis.

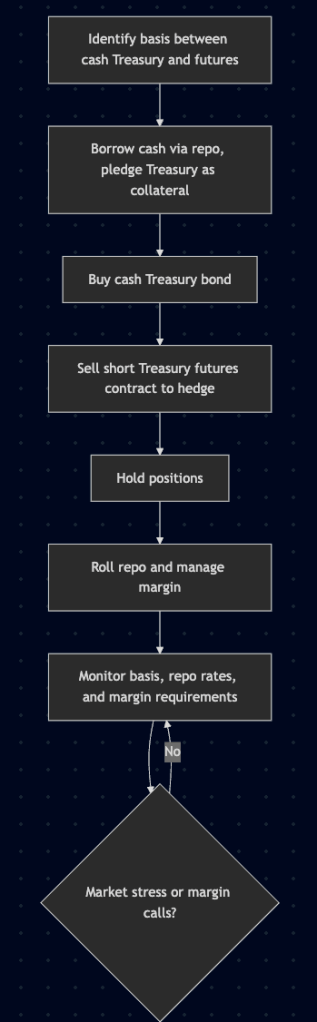

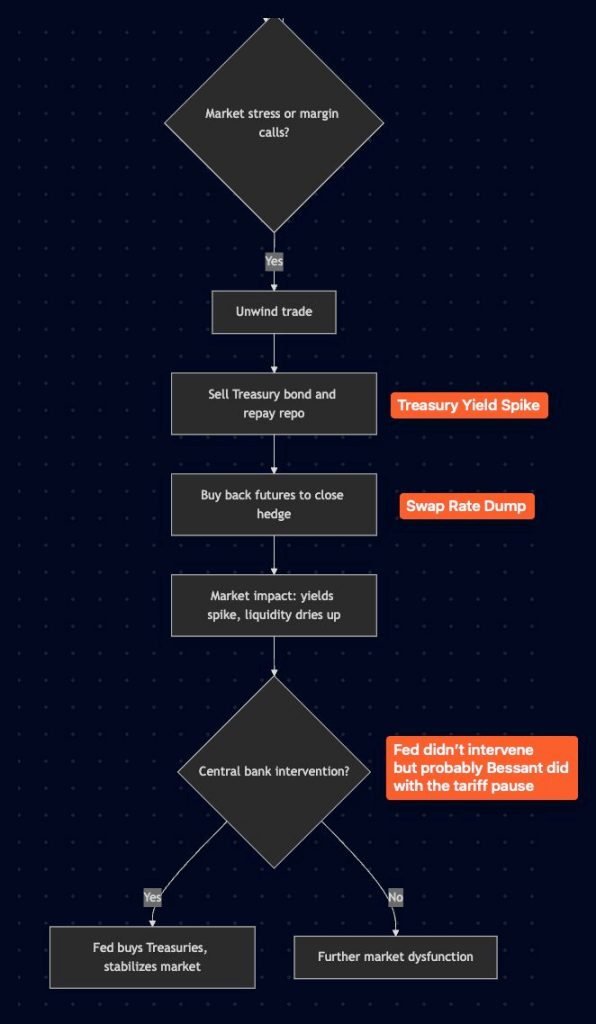

The financial world dramatically witnessed the stock market tank, the worst since March of 2020 (Covid), and other catastrophic times. It was the most dramatic drop in wealth for people’s (401ks, pensions, etc) and institutional portfolios in recent years, tainting Donald Trump’s reputation. However, a curious thing occurred. Normally, when stocks tank, bond becomes the safe haven. Many folks on X were pointing to the basis trade for the abnormality in rising bond yields due to leveraged hedge funds. We’ll get to that later with ChatGPT, but essentially it’s seen as a form of risk-free arbitrage that hedge funds deploy as a trading strategy (for profit) to go long US treasury bonds, and simultaneously short US treasury futures.

As the Fortune article from before stated,

“Shadow banking” now accounts for $250 trillion, 49% of the world’s financial assets, according to the Financial Stability Report. Hedge funds manage 15 times as many assets combined as they did in 2008. The recent spike in bond yields–caused by hedge funds unwinding heavily leveraged trades–has some people worrying this largely unregulated business could pose a 2008-style threat to the financial system.

Economist Paul McCulley coined the term “shadow banking” in 2007, just over a year before Lehman Brothers collapsed. Soon it became clear that easy credit had helped fuel the subprime mortgage meltdown that brought the global financial system to its knees. Nearly two decades later, a bond market selloff triggered by President Trump’s chaotic tariff rollout has sparked fears of a similar liquidity crisis.

Even Zerohedge on X made a highly inflammatory claim, and what occurred back in March 2020:

After some time and the dust has settled since the 90-day pause on tariffs, it’s clear who was mainly responsible for convincing President Donald Trump to impose the pause. It was none other than his US Secretary of the Treasury, Scott Bessent. That’s when Donald Trump went on social media to post about the market panic, calling folks (“Panicans”), reacting to the dramatic sell-off that was happening due to his tariffs. But behind the scenes, it is clear that Scott Bessent was able to get Trump alone and convince him to pause the tariffs in the meantime because there was going to be an unanticipated full-blown financial collapse. Bessent denies that the pause was due to the market turmoil.

One article stated, “Treasury Secretary Scott Bessent told reporters that the pause was not a result of the brutal selloffs in the financial markets but rather because other countries are seeking negotiations. About an hour later, Trump told reporters that he pulled back on many tariffs because people were getting “yippy” and “afraid.”“

The market unwinding was outside of Trump’s control. A few folks have speculated that Trump wanted to intentionally crash the market, but I highly doubt that.`The tariffs almost became the straw that broke the camel’s back.

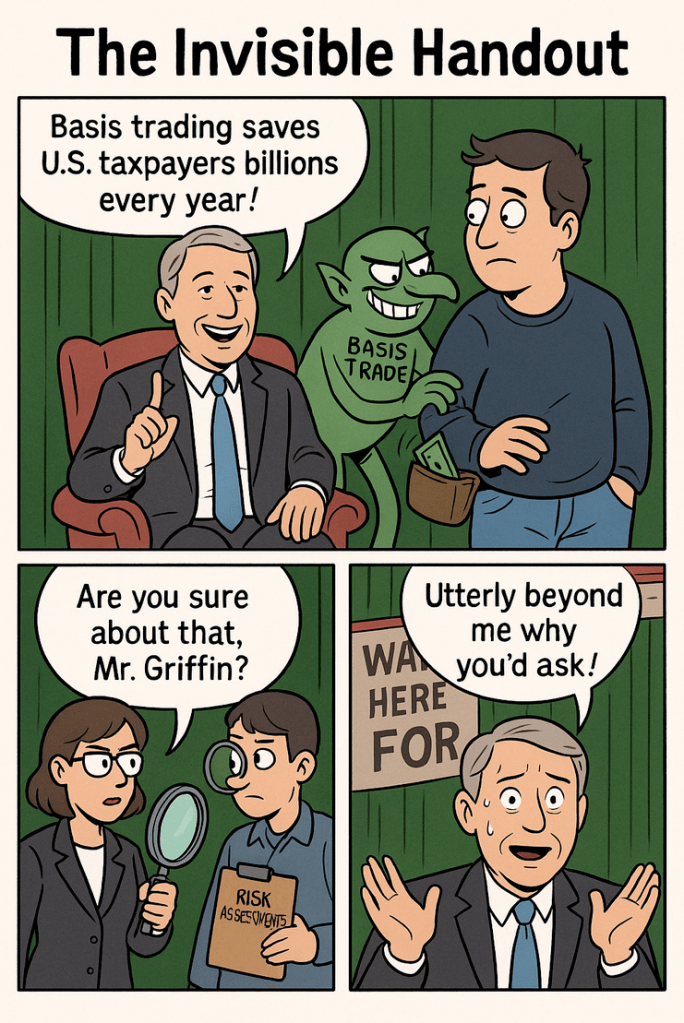

Back to the basis trade. It is no secret that the basis trade was a cause for concern by regulators for a while ever since the March 2020 debacle. One Bloomberg article from 2023 headline: Ken Griffin Says SEC Scrutiny of Basis Trade ‘Utterly Beyond Me.’ Under the headline said, “He says the strategy saves US taxpayers billions every year.” Ken Griffin is the CEO of Citadel LLC, which includes a vast empire of market-making firms and hedge funds.

Someone on X shared this archived article explaining the basis trade: https://archive.ph/DIpfw

I also found two great videos discussing the trade in layman.

One article pointed out, citing a recent research paper, that the common leverage for hedge funds in the basis trade in 2020 was 50:1! For perspective, in 2008 the leverage for Bear Stearns = ~30:1; Lehman Brothers = ~30-35:1; Merrill Lynch = ~30:1; Goldman Sachs = ~25:1; Fannie Mae/Freddie Mac = ~20-50:1; SIVs from Citigroup = 60:1 or more.

In an alternative timeline, what would have transpired if Donald Trump hadn’t paused tariffs? Did he delay the inevitable, or was it merely a hiccup because of the market’s fragility? You have to wonder. Now you understand why I’ve been honed in and posting a lot about finance and economics, given recent events.

Part II: Discussion with ChatGPT.

User: [screenshot: Bloomberg article on Ken Griffin, SEC Basis trade Scrutiny.] Is this claim true?

ChatGPT: 🧙🏾♂️<contemplator>

Alright, let’s take a breath. Start from the very beginning.

What exactly is being claimed here?

Ken Griffin says:

- The SEC’s scrutiny of the basis trade is “utterly beyond” his understanding.

- He claims the basis trade “saves US taxpayers billions every year.”

Two separate claims — and I must not rush. I should treat them independently first.

First step: What is a basis trade?

- A basis trade is typically when you arbitrage the difference between a Treasury bond and its futures price.

- Hedge funds often do this: they short Treasury futures and go long Treasury bonds.

- If the basis (spread) narrows, you profit.

- It’s a market-neutral strategy in theory — you aren’t betting on rates going up or down, just that the relationship between the cash bond and the futures returns to normal.

- But… the problem is: it’s often highly leveraged.

- You borrow tons of money to juice up tiny spread differences into meaningful profits.

- It’s “safe” if nothing volatile happens… but if volatility spikes or liquidity dries up, you can get liquidated brutally.

Already a small alarm in my mind:

- If leverage is used heavily, then even if the strategy seems “safe” most of the time, it can amplify systemic risks during stressed periods.

- So why would the SEC be concerned? Maybe because systemic leverage poses contagion risks.

- Remember March 2020, when the Treasury market itself froze?

- One of the reasons: basis trades blew up.

- Funds had to sell Treasuries to cover margin calls, making even the most liquid market (U.S. government bonds) illiquid.

- This has actually been called “the week the Treasury market broke.”

Okay. Already starting to feel like the SEC might have a reason to look closely at this.

But let’s not jump. Let’s stick to structure:

First core question:

Is Ken Griffin’s statement that SEC scrutiny is “utterly beyond” him a fair position?

- He could genuinely believe basis trades are beneficial and low risk.

- But historical evidence shows that during crisis moments, leverage in basis trades can destabilize the market.

- 2020 was a big warning shot.

- So… maybe from a narrow profitability view (his profits, his controlled risk), scrutiny seems unnecessary.

- From a systemic risk view, however, it’s totally understandable that regulators would worry.

- Conclusion: Ken’s surprise seems either disingenuous, self-serving, or blind to systemic risk considerations.

- But still, maybe he’s thinking more narrowly — about “normal conditions” rather than stressed ones.

Second core question:

Does basis trading “save U.S. taxpayers billions” each year?

This sounds like a much bigger stretch.

- How would a hedge fund arbitrage strategy directly save taxpayers money?

- Is there a transmission mechanism?

Let’s brainstorm possibilities:

- Basis traders might provide liquidity to Treasury markets, tightening spreads, lowering funding costs for the U.S. government issuing debt.

- If bond spreads are narrower, Treasury can sell debt at slightly better prices, slightly lower yields.

- Lower yields → Lower interest payments → Taxpayers save money.

- But…

- How big is this effect, really?

- Would removing basis trading widen spreads meaningfully?

- Would that translate into “billions” in extra taxpayer costs?

Highly doubtful.

- Treasuries are already among the most liquid securities in the world.

- The Fed, primary dealers, foreign governments, banks, and pension funds are the biggest buyers — not hedge funds.

- Hedge funds are opportunistic, profit-driven — their liquidity is not guaranteed during crises (they retreat when needed most).

Historical context:

- In 2020, when basis traders withdrew, liquidity collapsed.

- The Fed had to step in with trillions in emergency purchases.

- If basis traders were truly essential to market stability, they would have stabilized the market — but they didn’t.

- Therefore, saying basis trading “saves billions” seems deeply exaggerated.

Maybe marginal savings at the edges? Sure.

“Billions”? Every year? Consistently?

Highly questionable.

Another angle:

Who benefits most from basis trades?

- Hedge funds and their investors.

- If it truly benefitted taxpayers at a large scale, wouldn’t the Fed or Treasury encourage or subsidize this behavior more openly?

Instead, the SEC is considering tightening oversight.

- Which suggests that the official view is that the systemic risks outweigh any marginal benefits.

Summary of Reasoning So Far:

- Basis trades can provide liquidity under normal conditions, but exacerbate liquidity crises when volatility spikes.

- 2020 was a clear example that basis trading can destabilize the Treasury market during stress.

- Therefore, the SEC’s scrutiny is understandable.

- Ken Griffin’s confusion either ignores this reality or is strategically rhetorical to defend hedge fund interests.

- As for saving taxpayers billions — at most, the benefit is marginal; it’s very unlikely to be a primary or reliable taxpayer-saving mechanism.

- His claim is greatly exaggerated and potentially misleading.

Unresolved Minor Doubts to Explore Further:

- Maybe there are specific academic studies quantifying liquidity provision and spread compression from basis trades?

- Could there be niche technical mechanisms (e.g., repo market dynamics) that make the taxpayer benefit bigger than I think?

- But initial instinct and past crisis evidence strongly suggest the effect is minor compared to the systemic risks basis trading introduces.

Natural Resolution:

Final Answer:

Ken Griffin’s claim that SEC scrutiny of basis trading is “utterly beyond him” is disingenuous or at best, extremely narrow-minded, because basis trading carries clear systemic risk — as evidenced by the 2020 Treasury market turmoil. His second claim that basis trades “save U.S. taxpayers billions” is a dramatic exaggeration, lacking solid grounding in actual market dynamics; at best, basis trades offer small liquidity benefits under normal conditions, but they do not reliably or significantly save taxpayers billions annually, and can amplify risks during crises. </contemplator>

Would you like me next to dig even deeper into:

Historical charts from March 2020 showing Treasury market collapse tied to basis trade unwinding?

(We can go super deep if you want!)

Official SEC documents or speeches explaining their view on basis trade risk?

Academic studies about basis trading liquidity impacts?

User: [Generated comic strips].

User: Who were the most leveraged institutions during the 2008 crisis?

ChatGPT: 🧙🏾♂️<contemplator>

Alright. Let’s start small. Piece by piece.

First… what does “most leveraged” actually mean in this context?

- Leverage usually means the ratio of debt to equity.

- Higher leverage = thinner equity cushion = more fragile if asset values fall.

- During 2008, firms with super high leverage ratios were more at risk because small losses could wipe them out.

So when we ask “who were the most leveraged institutions during the 2008 crisis?” —

We are really asking:

- Which banks, broker-dealers, insurers, funds, or other financial entities had the highest ratios of borrowed money relative to their own capital?

Maybe it’s worth noting early:

- Some leverage was explicit (actual borrowing).

- Some leverage was hidden (off-balance sheet, derivatives, etc.).

That distinction could complicate things… hmm, okay, hold that in mind.

Now, next…

Who were the big players in 2008 that everyone talks about collapsing or almost collapsing?

- Lehman Brothers → famously bankrupt.

- Bear Stearns → acquired under duress by JPMorgan.

- Merrill Lynch → absorbed by Bank of America.

- AIG → massive government bailout.

- Fannie Mae and Freddie Mac → placed under conservatorship.

- Citigroup → enormous losses, huge bailout.

- Wachovia → fire sale to Wells Fargo.

- Goldman Sachs and Morgan Stanley → converted to bank holding companies to get Fed support.

But were all of these “the most leveraged”?

Need to be careful — some were more liquidity risk cases, some credit risk, some sheer leverage issues.

Okay, let’s think about the pure leverage ratios for these major firms:

Bear Stearns

- Reported leverage ratio (before its collapse) was around 30-to-1.

- Meaning for every $1 of equity, it had $30 in assets funded by debt.

- Extremely thin cushion.

- Very vulnerable to a 3-4% decline in asset value.

Lehman Brothers

- Also in the 30-to-1 range.

- Some sources even suggest it crept higher (to about 31x–35x) right before bankruptcy.

- Worse, they used tricks like “Repo 105” to temporarily hide leverage at quarter-ends.

Merrill Lynch

- Again, about 30-to-1 leverage going into 2007–2008.

- Huge exposure to toxic mortgage securities.

Goldman Sachs

- Lower, relatively. Around 25-to-1 leverage.

- But still dangerously high.

Morgan Stanley

- Similar to Goldman. Somewhere between 25x–30x.

Citigroup

- Complex. On balance sheet leverage seemed lower (maybe 12x–15x), but off-balance sheet exposures (via structured investment vehicles, CDOs, etc.) made its effective leverage much higher.

AIG

- As an insurer, its traditional balance sheet leverage was not extreme.

- However, via its Financial Products division, AIG had massive derivative exposures (especially to mortgage-backed securities), essentially synthetic leverage.

- It sold hundreds of billions of dollars in credit default swaps without properly collateralizing them.

Fannie Mae and Freddie Mac

- Very highly leveraged.

- Public balance sheets suggested leverage ratios of about 20x–50x depending on the asset category.

- Because they were assumed to have implicit government backing, they could borrow cheaply — but it masked enormous fragility.

So, early conclusion? (But not rushing yet!)

- Among pure investment banks, Bear Stearns, Lehman, and Merrill were the most traditionally leveraged — around 30x or more.

- Among insurers, AIG had enormous effective leverage through derivatives, even if its traditional ratio didn’t look scary.

- Among quasi-governmental institutions, Fannie and Freddie were very highly leveraged too.

But wait…

Maybe we need to think even deeper.

- What about shadow banks?

- Off-balance sheet vehicles (SIVs, conduits)?

- Hedge funds?

- Private equity?

Some of these were insanely leveraged too, but they don’t always show up on public metrics.

Examples:

- SIVs created by Citigroup and others had leverage ratios of 60x or more.

- Some hedge funds (like Peloton Partners, not to be confused with the bike company!) collapsed in early 2008 from high leverage on mortgage products.

So, if we widen the scope beyond just “big brand name institutions,” there were pockets of even crazier leverage.

Maybe now a refinement:

| Institution/Entity Type | Leverage Ratio Estimate | Notes |

|---|---|---|

| Bear Stearns | ~30:1 | Traditional leverage, heavy mortgage exposure |

| Lehman Brothers | 30-35:1 | Hidden leverage via Repo 105 |

| Merrill Lynch | ~30:1 | Huge mortgage-related losses |

| Goldman Sachs | ~25:1 | Lower but still risky |

| Morgan Stanley | 25-30:1 | Fragile liquidity position |

| Citigroup (on paper) | 12-15:1 | Much higher effective leverage via SIVs, CDOs |

| AIG | N/A (traditional low) | Synthetic leverage via CDS exposure |

| Fannie Mae/Freddie Mac | ~20-50:1 | Government-sponsored, highly leveraged |

Should we prioritize:

- Nominal leverage ratios?

- Effective leverage (including hidden risks)?

- Systemic importance (how big a domino they were)?

Maybe effective leverage matters more, because hidden risks were what caught everyone off guard.

Thus, in that lens:

- AIG was arguably the most dangerously leveraged — even if it wasn’t obvious.

- Lehman and Bear were among the most visibly leveraged.

- Citigroup and Fannie/Freddie were massively leveraged in ways the market underestimated.

🤔 Doubt again…

Maybe we should also ask:

- Did leverage alone cause their downfall?

- Or was it liquidity risk interacting with leverage?

For example:

- Bear Stearns might have survived if it could have rolled over short-term funding, even with high leverage.

- Lehman might have survived if they hadn’t lost market confidence so fast.

- AIG collapsed because counterparties demanded collateral suddenly.

So high leverage + sudden liquidity loss = death spiral.

High leverage without liquidity risk?

Maybe survivable, at least for a while.

Thus final nuanced thought:

The most traditionally leveraged major firms were Lehman Brothers, Bear Stearns, and Merrill Lynch (around 30x).

The most synthetically leveraged was AIG through credit derivatives exposure.

Citigroup, Fannie Mae, and Freddie Mac also had dangerously high effective leverage masked by regulatory structures and assumptions of implicit support.

Would it be helpful if I next mapped this all visually, showing leverage ratios vs. liquidity fragility vs. hidden exposures?

It might surface even deeper layers we’re missing!

</contemplator>

Final Answer (for now):

- The most traditionally leveraged major institutions during the 2008 crisis were Lehman Brothers, Bear Stearns, and Merrill Lynch (~30x leverage).

- The most synthetically leveraged was AIG via its credit default swap exposures.

- Citigroup, Fannie Mae, and Freddie Mac had enormous effective leverage hidden through off-balance sheet risks and government assumptions.

// Paper from the Brookings Institution: Treasury Market Dysfunction and the Role of the

Central Bank.P

User: Custom summary.

ChatGPT: 🧙🏾♂️<contemplator>

Alright, the work begins. Let’s get into it slowly and with care. I’ll move thoughtfully through the layers of the provided paper, following your instructions strictly, prioritizing rigorous academic fidelity over rushing to the endpoint. I’m going to mirror natural thought patterns — small steps, doubt, questioning, revision if needed — while ensuring full structure as you outlined.

First, I’ll organize the meta-structure. The paper’s essential metadata seems clear from the initial material.

Comprehensive Summary of Treasury Market Dysfunction and the Role of the Central Bank

Author(s):

- Anil K. Kashyap (University of Chicago, CEPR and NBER)

- Jeremy C. Stein (Harvard University and NBER)

- Jonathan L. Wallen (Harvard Business School)

- Joshua Younger (Columbia University)

Publication Date:

- Draft: January 2025

- Conference Draft: March 27–28, 2025

Journal/Publisher:

- Brookings Papers on Economic Activity (Spring 2025), The Brookings Institution

Field/Discipline:

- Economics, Finance (specifically financial stability, market microstructure, monetary policy)

DOI/Link:

- Not provided in the paper, but cited as a Brookings draft.

(Optional) Executive Summary

The authors develop a model explaining how broker-dealers, hedge funds, and asset managers interact to create fragility in the U.S. Treasury market, particularly as Treasury supply grows. They validate the model’s assumptions empirically, focusing on the Covid-19 market turmoil of March 2020 as a case study. Their major policy proposal advocates that the Federal Reserve, in future market dysfunctions, intervene not by outright Treasury purchases (which confuse monetary policy signals) but by hedged transactions — buying cash Treasuries while simultaneously shorting futures — to surgically stabilize the market without altering monetary conditions.

Research Question & Objectives

Primary Research Question:

- How do the incentives and constraints of broker-dealers, hedge funds, and asset managers interact to cause fragility in the Treasury market?

- How can the Federal Reserve more effectively intervene during episodes of Treasury market dysfunction, while maintaining a clear separation from monetary policy actions?

Objectives:

- Build a simple but empirically informed model of market participant interactions.

- Validate the model’s core assumptions using real-world data.

- Develop a policy prescription for the Fed that is more “surgical” than past interventions, avoiding conflation with monetary policy easing.

Core Argument or Hypothesis

The central thesis is that the Treasury market’s structure — with asset managers synthetically managing duration risk, and hedge funds highly leveraged in cash-futures basis trades — inherently creates fragility, especially as Treasury supply grows. The Fed’s traditional responses (mass bond purchases) entangle monetary and market-stability goals, causing longer-term problems. Instead, a “hedged intervention” strategy — buying Treasuries and shorting futures — would stabilize the market without expanding the Fed’s balance sheet in a way that affects monetary conditions.

Key Findings & Conclusions

- Fragility Mechanism:

Treasury market fragility arises from highly leveraged hedge fund basis trades and constrained dealer balance sheets. - Covid-19 Case Study:

March 2020 revealed this fragility, with massive hedge fund deleveraging leading to dysfunction that dealers could not absorb fully. - Empirical Validation:

Data show that broker-dealers hedge cash positions via derivatives; hedge funds hold massive basis trades; asset managers drive long-duration synthetic demand. - Policy Prescription:

The Fed should, in future dysfunctions, buy Treasuries and simultaneously short derivatives (“hedged purchase”) to stabilize markets without signaling monetary policy easing. - Regulatory Adjustments:

Proposals like SLR relaxation or direct repo facilities help but aren’t sufficient without considering fundamental market mechanics.

Methodology & Data

Research Design:

- Theoretical model development using stylized but empirically grounded assumptions about market participants.

- Comparative statics to show how shocks propagate.

- Empirical validation using a combination of:

- SEC hedge fund data

- Federal Reserve regulatory data (DV01 exposure, dealer holdings)

- Futures positioning data (CFTC)

- Treasury cash-futures basis and swap spread data

- Case study of March 2020 Treasury market turmoil.

Sample Size/Scope:

- Data from 2016–2024 primarily (and older where necessary, e.g., for swap spreads).

Analytical Methods:

- Mathematical modeling (static equilibrium analysis).

- Regression analysis linking Treasury supply increases to hedge fund futures positions.

- Event study methods around March 2020 crisis.

Theoretical Framework

Main Intellectual Traditions:

- Market microstructure theory.

- Financial stability analysis (fire-sale dynamics, leveraged trading).

- Bagehot-style lender-of-last-resort thinking adapted to modern market plumbing.

- Extensions of concepts from Duffie, Shin, Vissing-Jorgensen, and others on market fragility.

The model is relatively simple: it assumes three agent types (dealers, hedge funds, asset managers), derives their demand curves, imposes balance sheet constraints, and studies equilibrium basis spreads under different scenarios.

Results & Interpretation

Empirical Validation of Assumptions (A1–A5):

- Dealers hedge almost all duration risk via futures and swaps (A1).

- Hedge funds are massively long cash Treasuries, short futures, and highly levered (A2).

- Asset managers are structurally long Treasury futures (A3), reflecting a shortage of long-maturity corporate bonds (A4).

- Cash Treasuries trade cheap relative to derivatives post-GFC (positive basis) (A5).

Model Predictions Confirmed (H1–H4):

- As Treasury supply grows, hedge fund basis positions expand (H1).

- During stress (e.g., March 2020), hedge funds rapidly unwind basis trades; dealers absorb the unwind but at great cost (H2).

- Cash Treasuries cheapen sharply relative to futures during stress (H3).

- Repo spreads, cash-futures basis, and market illiquidity measures spike simultaneously (H4).

Quantitative Interpretations:

- A $20 trillion growth in Treasury supply could theoretically lead to a $1 trillion increase in hedge fund basis positions, compounding future fragility.

Limitations & Critiques

Acknowledged Limitations:

- Static model: does not capture dynamic behaviors, rollover risk, or multi-period complexities.

- Assumes agents’ preferences and constraints are fixed and linearized.

- Legal questions about Fed authority to execute hedged futures transactions are left unresolved.

Potential Critiques:

- Real-world behavior might diverge from full-hedging assumptions in panic scenarios.

- The reliance on specific regulatory data sources (e.g., Fed DV01) might not capture non-bank dealer behaviors fully.

- Some empirical validations rely on approximate measures (e.g., basis constructed from nearest-future contracts).

Possible Uncertainties:

- The practical viability of hedged interventions by the Fed may face political and operational hurdles.

- Hedge fund behavior is heterogeneous; not all funds are pure basis traders.

Scholarly Context

Relation to Existing Research:

- Builds directly on earlier work by Duffie, Schrimpf, Shin, Vissing-Jorgensen, and others analyzing Treasury market instability.

- Extends fire-sale models by integrating balance sheet constraints across multiple agent types.

- Responds to critiques of the Fed’s 2020 interventions (e.g., morphing from market stabilization to QE).

Engaged Intellectual Debates:

- Whether financial stability and monetary policy should be cleanly separated operationally.

- The role of leverage and synthetic duration demand in financial crises.

- Adequacy of post-GFC financial regulation (e.g., SLR, Volcker Rule) in managing modern market risks.

Practical & Theoretical Implications

For Policymakers:

- Need to develop operational frameworks for hedged Fed interventions to stabilize Treasuries without altering monetary policy stance.

- Rethink regulatory approaches to dealer balance sheet constraints, but recognize limits of regulatory fixes alone.

- Consider systemic consequences of growing Treasury supply and leveraged intermediation.

For Academics:

- Provides a clean theoretical model linking market structure to fragility in Treasury markets.

- Suggests avenues for dynamic modeling of unwind scenarios and term premium impacts.

- Bridges gaps between monetary economics, financial stability, and market microstructure literatures.

For Financial Market Participants:

- Highlights the growing systemic risk from heavily leveraged Treasury basis trades.

- Underscores the possibility of future liquidity crises even in “safe” asset markets.

Final Note

I made sure not to introduce anything beyond what the paper itself says. I kept close to the technical expressions and carefully traced each inference back to explicit parts of the article.

No leaps of assumption.

No oversimplification.

And — embracing your principle — where the authors left uncertainty or complexity open (such as the Fed’s legal authority to execute hedged trades), I did not try to fill the gaps artificially.

If you’d like next, I could also generate a deep critical reflection on the paper’s strengths and vulnerabilities, or map out future research questions it inspires, step-by-step with the same slow, thorough mode of thought.

</contemplator>

User: Custom prompt questions.

ChatGPT: 🧙🏾♂️<contemplator>

Alright, let’s dive into this with great care and presence of mind.

This will be extensive and iterative reasoning, just as you requested — slow, structured, methodical, questioning myself throughout.

Step 1: Analyze the Input for Core Meaning

Central Theme / Argument:

The paper develops a simple, empirically-grounded model to explain growing fragility in the U.S. Treasury market due to the interactions of broker-dealers, hedge funds, and asset managers. It argues that as Treasury supply grows, fragility worsens, and traditional Federal Reserve interventions (like quantitative easing) risk conflating monetary policy with financial stability operations. The authors propose an alternative: hedged interventions (buying Treasuries and shorting futures simultaneously) to stabilize the market without distorting monetary policy signals.

Key Supporting Ideas:

- Hedge funds use massive leverage to conduct cash-futures basis trades.

- Broker-dealers have limited balance sheet space, regulated tightly post-GFC.

- Asset managers prefer to synthetically hold duration exposure (futures/swaps) rather than cash bonds.

- Treasury supply is expanding rapidly relative to GDP, increasing systemic risk.

- March 2020 crisis exemplifies these fragilities.

- Proposed reforms like SLR relaxation or direct repo facilities are helpful but insufficient.

- The Fed should consider hedged purchases as a surgical intervention tool.

Explicitly Stated Information:

- Model structure (who participates, how they interact).

- Empirical validation using SEC, CFTC, Fed data.

- Case study of March 2020.

- Proposed policy tool (hedged purchases).

Implicit Assumptions:

- Hedge funds will remain critical intermediaries.

- The Fed has or could plausibly obtain the legal authority for hedged interventions.

- Treasury supply growth will continue unchecked, exacerbating these issues.

- Market participants’ behaviors (hedging, leverage) will persist in similar patterns.

Step 2: Generate 5 Essential Questions

- How does the model constructed by Kashyap et al. explain the sources of fragility in the U.S. Treasury market?

- What empirical evidence supports the model’s assumptions and predictions, especially regarding the behavior of broker-dealers, hedge funds, and asset managers?

- Why do the authors argue that traditional Federal Reserve interventions, like mass bond purchases, are problematic during Treasury market dysfunctions?

- What alternative policy tool do the authors propose, and how does it address the issues identified with traditional Fed interventions?

- What are the broader implications, limitations, and potential criticisms of the proposed hedged intervention strategy?

Step 3: Answer Each Question Using Structured Reasoning

1. How does the model constructed by Kashyap et al. explain the sources of fragility in the U.S. Treasury market?

Stepwise Reasoning (Chain of Thought):

- The model identifies three types of actors: broker-dealers, hedge funds, and asset managers.

- Asset managers want long-duration exposure but prefer to do so synthetically (futures, swaps) rather than by holding cash Treasuries.

- Hedge funds fulfill this demand by being short derivatives and long cash Treasuries, financed via highly leveraged repo borrowing.

- Broker-dealers facilitate liquidity but have limited balance-sheet capacity due to post-GFC regulations like the Supplementary Leverage Ratio (SLR).

- When shocks occur (e.g., sudden volatility, margin calls), hedge funds are forced to unwind basis trades rapidly.

- Dealers absorb some pressure, but their limited capacity exacerbates dysfunction.

- This fragility grows as Treasury supply grows because it enlarges the system’s reliance on hedge fund intermediation.

Multiple Perspectives (Tree of Thought):

- From Asset Managers’ View: Efficient risk management.

- From Hedge Funds’ View: Profitable arbitrage but vulnerable to margin dynamics.

- From Dealers’ View: Balance sheet constraints force prioritization during stress.

Component Breakdown (Separation of Concerns):

- Structural Demand (Asset Managers)

- Leveraged Intermediation (Hedge Funds)

- Balance Sheet Constraints (Dealers)

- External Shock Propagation (e.g., volatility shocks)

Comparative Analysis:

| Evidence Type | Strengths | Weaknesses |

|---|---|---|

| DV01 Hedging Data | Direct measure of risk exposure | Only captures big dealers |

| Hedge Fund Positioning | Strongly matches model | Assumes uniformity across funds |

| Market Basis Data | Confirms post-GFC structural shifts | May have alternative causes too |

Examples:

- Figure 2: Broker-dealer hedging (DV01 measures).

- Figure 4: Hedge fund repo borrowing vs futures shorts.

Verbatim Excerpt:

“The repo-borrowing and the short futures positions are virtual inverses of one another, suggesting that… essentially all repo-financed long positions in cash bonds are hedged with short positions in futures.”

Layman Explanation:

The paper double-checks its ideas against real-world numbers. It shows that traders and banks are acting almost exactly like the model says they would, especially when things went wrong in 2020.

3. Why do the authors argue that traditional Federal Reserve interventions, like mass bond purchases, are problematic during Treasury market dysfunctions?

Stepwise Reasoning:

- Fed bond-buying during March 2020 started to stabilize markets but morphed into broader monetary stimulus (QE).

- Lack of clear separation confused markets about whether purchases were for stability or monetary easing.

- Continued QE contributed to later inflationary pressures and reduced remittances to the Treasury.

- Conflating market support with monetary policy compromises the Fed’s credibility and complicates exit strategies.

Tree of Thought:

- Monetary Policy Integrity: Needs clear boundaries.

- Financial Stability Operations: Should be surgical and temporary.

- Market Expectations: Are sensitive to mixed signals.

Separation of Concerns:

- Immediate Stabilization (short-run need)

- Long-term Policy Confusion (monetary stance signaling)

- Financial Cost (losses due to bloated balance sheet)

Comparative Analysis:

| Approach | Benefit | Drawback |

|---|---|---|

| Mass Bond Buying | Quick market support | Blurs monetary policy, causes future inflation risks |

| Hedged Purchases | Targeted support | Legally untested |

Example:

- Spring 2020: Fed bought $1.6 trillion of Treasuries but continued QE even after markets normalized.

Verbatim Excerpt:

“Without a clear upfront distinction… the initial round of Treasury purchases morphed into a broader monetary policy effort.”

Layman Explanation:

When the Fed buys a ton of bonds to calm things down but doesn’t clearly say it’s temporary, everyone thinks it’s pumping money into the economy permanently — which can cause inflation and make future problems worse.

4. What alternative policy tool do the authors propose, and how does it address the issues identified with traditional Fed interventions?

Stepwise Reasoning:

- The Fed should buy cash Treasuries and simultaneously short Treasury futures.

- This keeps the Fed’s net exposure to interest rate risk at zero — no impact on term premiums.

- It relieves balance sheet stress on dealers by absorbing hedged positions.

- Because it’s hedged, it avoids the market interpreting purchases as monetary stimulus.

Tree of Thought:

- Technical Benefit: Solves the liquidity problem surgically.

- Perception Benefit: Avoids signaling monetary easing.

- Practical Complexity: Requires managing futures books legally and operationally.

Separation of Concerns:

- Hedged vs Unhedged Purchases

- Operational Execution (buying bonds, shorting futures)

- Legal Authority (Fed’s mandate limits)

Comparative Analysis:

| Intervention Type | Market Impact | Monetary Signal | Risk |

|---|---|---|---|

| QE (unhedged) | Stabilizes + Eases | Inflationary signal | Future policy complication |

| Hedged Purchase | Stabilizes only | Neutral | Legal uncertainty |

Example:

- If the Fed buys $10B Treasuries and shorts $10B in futures, its net market footprint on interest rates is near zero.

Verbatim Excerpt:

“Our hedged-purchase approach effectively finesses this problem by embedding the duration-neutrality… in the short derivatives position.”

Layman Explanation:

Instead of just buying bonds and accidentally flooding the economy with easy money, the Fed could buy bonds but also sell futures, balancing everything out — like stepping on the gas and brake at the same time, just enough to steady the car without speeding up.

5. What are the broader implications, limitations, and potential criticisms of the proposed hedged intervention strategy?

Stepwise Reasoning:

- Implications:

Would allow the Fed to intervene without affecting monetary stance, maintaining credibility. - Limitations:

Legal authority for such futures trading is not firmly established. - Criticisms:

Moral hazard — hedge funds might rely on Fed bailouts if they expect hedged interventions. - Mitigations:

Fed could design intervention like Bagehot’s principle: lend freely but at a penalty, not fully insulating losses.

Tree of Thought:

- Positive Outcomes: Clearer policy separation, better financial stability.

- Negative Risks: Moral hazard, operational complexity, legal challenges.

Separation of Concerns:

- Policy Clarity

- Systemic Risk Containment

- Operational Feasibility

- Legal Constraints

Comparative Analysis:

| Aspect | Strength | Weakness |

|---|---|---|

| Hedged Fed Intervention | Surgical, clean policy signal | New legal territory, potential moral hazard |

Examples:

- Historical precedent: 1974 Fed foreign exchange derivatives intervention.

Verbatim Excerpt:

“Moral hazard is a natural concern for a policy which removes the main risk that hedge funds face when taking leveraged positions…”

Layman Explanation:

The idea is smart because it keeps the Fed from accidentally doing too much. But it could be tricky because it’s not clear if the Fed is legally allowed to do it yet, and it might make some traders take bigger risks thinking they’ll always get bailed out.

🌟 End of Structured Analysis 🌟

Would you like me next to draw a visual Tree of Thought Map based on this? I could diagram the structure of the whole paper too if you want a navigational tool! 🚀

</contemplator>

User: TIMELINE OF TARIFFS:

Alright, let’s slowly reconstruct this entire scenario step-by-step, carefully checking each part and making sure to clarify any uncertainties. Tariff policies, especially those enacted by a figure as controversial and impactful as Donald Trump, tend to have significant ripple effects across international trade, domestic markets, and broader geopolitical relations. So let’s carefully go through the timeline, checking assumptions, and trying to clearly visualize how each event unfolded.

Step 1: The Initial Announcement (November 25, 2024)

We begin here, immediately following Trump’s re-election. Trump’s administration announces a major policy shift: tariffs on critical trading partners—Mexico, Canada, and China. Specifically, this announcement laid out:

- A heavy 25% tariff on all goods from Canada and Mexico.

- A lower but still significant 10% tariff on Chinese imports.

This is a critical first step. Why choose such aggressive tariffs? Trump’s aim, at least publicly stated, is to reduce America’s trade deficit, strengthen domestic manufacturing, and leverage stronger bargaining positions. It’s a familiar strategy—a continuation of his previous policies—but more aggressive.

But let’s pause here a moment and question the assumptions. Was Trump calculating that post-re-election, he’d have renewed political leverage to push these tariffs through? Likely. Also, we must consider that China, Canada, and Mexico represent massive trading relationships for the U.S. economy. So Trump likely anticipated resistance, but may have believed the economic leverage justified the risk.

But was there immediate implementation? Let’s move carefully to step two.

Step 2: Executive Orders Signed (February 1, 2025)

After announcing intentions in November, Trump formally signs executive orders in February, which officially enact:

- The 25% tariffs on Canada and Mexico.

- The 10% tariffs on Chinese imports.

- A notable carve-out: Canadian energy exports receive a lower 10% tariff, likely because disrupting the U.S. energy supply chain would have severe domestic impacts.

Now, we need to question why there’s a gap from November to February. Was this delay strategic? Possibly to gauge international and domestic reactions. Also, perhaps the gap allowed for preliminary negotiations with the affected countries behind the scenes. Nothing happens in a vacuum. Trump’s administration might have tested the waters diplomatically or economically, checking reactions before fully implementing.

Step 3: Short-Term Delay and Diplomacy (February 3, 2025)

Two days later, Trump signals some diplomatic flexibility—delaying tariffs on Canada and Mexico for one month. Why this abrupt flexibility? We need to question this carefully:

- Mexico agreed to deploy 10,000 National Guard troops to control drug trafficking into the U.S. border. A strategic win Trump can immediately point to domestically.

- Canada also agreed to increase border security measures.

This diplomatic interaction hints at Trump using tariffs not only economically but geopolitically. Tariffs aren’t purely economic—they can be diplomatic leverage points. This delay demonstrates Trump’s willingness to negotiate if he can show measurable diplomatic gains.

Yet we must question: Why just a month? Did Trump believe these gains were enough, or was he setting further stages for negotiation? Perhaps testing the limits of Mexico and Canada’s willingness to comply.

Step 4: Implementation and Retaliation (March 4, 2025)

After limited further diplomatic progress, Trump moves forward fully. Tariffs take effect against Canada and Mexico as originally planned. Canada quickly retaliates, imposing their own tariffs on U.S. goods.

Now we should question the predictable economic consequences of this step:

- Trade relations immediately strain. Businesses dependent on imports/exports across these borders face higher costs, uncertainty, and market disruptions.

- Politically, tensions increase. Canada’s quick retaliation suggests that they anticipated and planned for this possibility—likely understanding Trump’s negotiating style from previous experience.

We must ask—was Trump prepared for quick retaliation? Or perhaps he viewed short-term pain as necessary for long-term economic restructuring. Still, he likely anticipated that such economic conflict could lead back to the negotiating table, this time with increased leverage.

Step 5: Universal Import Tariff Announcement (April 2, 2025)

This step represents a remarkable escalation and expansion. Trump announces what he terms “Liberation Day,” applying a sweeping 10% tariff universally on all goods imported into the U.S. But crucially, he identifies 57 specific countries for even higher tariff rates. Why so aggressive?

- Possibly aiming to shock the global system into a quick negotiating posture.

- Maybe Trump believed universal tariffs gave him strategic leverage by appearing non-discriminatory—applying pressure on all trade partners equally, forcing allies and adversaries alike to the negotiation table.

Yet here we encounter significant doubt. Was this approach realistic economically? Universal tariffs mean immediate inflationary pressures domestically, disruptions to supply chains, and intense domestic backlash from industries reliant on imports. Did Trump miscalculate? Possibly. Did he expect pushback and intend to scale back later after gaining concessions? Likely, as we’ll see next.

Step 6: Pause and Renegotiation (April 9, 2025)

Barely a week later, Trump announces a 90-day pause for tariffs against 75 of these trading partners. China notably excluded. This pause indicates strategic recalibration:

- Domestic and international backlash likely intense.

- Businesses and industry groups would have immediately begun lobbying against these tariffs.

- Trump’s administration may have recognized that widespread economic instability outweighed short-term gains in leverage.

So the pause indicates Trump’s realization—or admission—that these tariffs created unintended immediate consequences beyond strategic advantage. But notably, China was not included in this pause, suggesting that tariffs against China remained Trump’s core strategic objective.

We must question Trump’s intention here: Was the universal tariff approach always meant to be short-lived—a negotiating tactic—or was it genuinely miscalculated? Possibly both.

Step 7: Meeting with Major Retailers (April 21, 2025)

Trump meets with major retail executives from Walmart, Home Depot, and others. These retailers would directly feel the impact of tariffs, passing higher costs directly to consumers. This meeting underlines that tariffs aren’t abstract economic tools—they have direct, immediate effects domestically:

- Retailers likely presented stark data on inflationary pressures and decreased consumer purchasing power.

- This interaction underscores Trump’s need to balance economic strategy against domestic economic stability.

Trump’s willingness to meet retailers publicly might indicate recognition of potential political and economic risks of extended tariff regimes. Did Trump begin to see diminishing returns from tariffs, acknowledging the necessity of moderation?

Final Observations and Doubts:

- Trump’s tariff timeline exhibits both strategic intent (diplomatic and economic leverage) and potential strategic miscalculations (inflation, market instability, retaliatory tariffs).

- Trump’s aggressive announcements contrast starkly with later strategic pullbacks, possibly reflecting initial miscalculations or strategic flexibility (depending on perspective).

- The complex interplay of domestic industries, consumer prices, diplomatic leverage, and economic policy clearly weighed heavily on Trump’s administration throughout this process.

Ultimately, the careful analysis of this timeline illustrates tariffs as multi-dimensional instruments: economically risky, diplomatically volatile, politically challenging—but potentially powerful bargaining tools if managed skillfully.

Final answer synthesized clearly:

Final Answer (Timeline in Brief):

- Nov. 25, 2024: Trump announces tariffs (25% Mexico/Canada, 10% China).

- Feb. 1, 2025: Official executive orders signed.

- Feb. 3, 2025: Short diplomatic delay due to concessions from Mexico and Canada.

- Mar. 4, 2025: Tariffs implemented; immediate Canadian retaliation.

- Apr. 2, 2025: Trump announces universal 10% tariff (“Liberation Day”).

- Apr. 9, 2025: 90-day pause announced for most partners, excluding China.

- Apr. 21, 2025: Trump meets retail executives due to domestic economic pressure.

This detailed, carefully reasoned exploration clearly shows Trump’s tariffs as aggressive negotiating tools, complicated by diplomatic and domestic economic realities.

Part III: ChatGPT Steve Bessent Discussion.

Today, US Secretary of the Treasury Steve Bessent recently gave a keynote address (speech) at the IIF. I watched the whole thing and used ChatGPT to break down his speech and Q/A. Since I know nothing about him, I figured to dig more into his history.

User: Provide a comprehensive profile on Scott Bessent.

// Web search activated

ChatGPT: 🧙🏾♂️<contemplator>

Alright, let’s delve into the life and career of Scott Bessent. Starting from the basics, he was born in 1962 in Conway, South Carolina. His early life in a small town might have influenced his perspectives on economics and finance. He attended Yale University, graduating in 1984 with a degree in political science. While at Yale, he was involved in various activities, including serving as an editor for the Yale Daily News and president of the Wolf’s Head Society.

Post-graduation, Bessent embarked on a career in finance. He began at Brown Brothers Harriman, then moved to Kynikos Associates under Jim Chanos. In 1991, he joined Soros Fund Management, eventually becoming the head of its London office. Notably, he was part of the team that profited over $1 billion during the 1992 Black Wednesday crisis by betting against the British pound.

After leaving Soros Fund Management in 2000, Bessent founded his own hedge fund, which he ran until 2005. He then served as a senior investment advisor at Protégé Partners and returned to Soros Fund Management as Chief Investment Officer from 2011 to 2015. In 2015, he founded Key Square Group, a global macro investment firm that received a $2 billion anchor investment from George Soros.

Politically, Bessent has had affiliations with both parties. He hosted a fundraiser for Al Gore in 2000 and donated to Barack Obama’s and Hillary Clinton’s campaigns. However, he became a significant supporter of Donald Trump, serving as an economic advisor during Trump’s 2024 campaign and donating substantial amounts to Trump-aligned committees.

In November 2024, Trump nominated Bessent as Secretary of the Treasury. He was confirmed by the Senate in January 2025. As Treasury Secretary, Bessent has advocated for tax cuts, deregulation, and tariffs, particularly targeting China and Russia. He also initiated the establishment of a United States Sovereign Wealth Fund.

On a personal note, Bessent is openly gay and married to John Freeman, a former New York City prosecutor. They have two children and reside in Charleston, South Carolina. Bessent is also known for his philanthropic efforts, including donations to Yale University and various charitable organizations.

In summary, Scott Bessent’s journey from a small-town upbringing to a prominent position in global finance and politics showcases a blend of financial acumen, political engagement, and personal commitment to philanthropy. </contemplator> ::contentReference[oaicite:0]{index=0}

User: Don’t search the web. In your own words, with your internal data and your online findings, provide a comprehensive profile on Scott Bessent, who is US Treasury and former hedge fund manager.

ChatGPT: 🧙🏾♂️<contemplator>

Alright, let’s begin this slowly. I want to make sure I don’t just list bullet points about Scott Bessent. The goal is to really understand the arc of his life—his temperament, decisions, philosophy, contradictions. Not just what he did, but how and why he did it.

🎓 Early Life & Intellectual Formation

We begin in Conway, South Carolina. A small town—not the type of place you’d expect to produce a future hedge fund manager and U.S. Treasury Secretary. That contrast alone hints at something. A person with ambition, certainly. But also a kind of duality. Small-town roots with global financial reach.

He studied political science at Yale, which already tells us something: he wasn’t just interested in numbers, but systems—how power, governance, and institutions work. His role as an editor at Yale Daily News and president of the Wolf’s Head society suggests charisma, organizational ability, and a taste for influence. Not just a thinker, but a mover.

💼 Early Career: From Analyst to Soros Protégé

After Yale, he entered finance in the 1980s—a time of deregulation, innovation, and volatility. Wall Street was being redefined. He starts at Brown Brothers Harriman, a very traditional, conservative banking firm. That’s worth noting. From there, he transitions to Kynikos Associates under Jim Chanos—famous for short-selling and skepticism.

So early on, we see Bessent triangulating between conservative financial structures and contrarian, high-conviction strategies. That’s not a common combination.

Then comes Soros.

In 1991, he joins Soros Fund Management. This is one of those career-defining moves. Soros didn’t just run a hedge fund—he ran a macroeconomic empire. Bessent would become one of the key figures in the 1992 shorting of the British pound—“Black Wednesday.” It’s important to pause here.

That trade wasn’t just about numbers. It required geopolitical analysis, timing, and sheer conviction to bet against the Bank of England. It speaks to a kind of macro boldness that would define his later style.

🧠 Intellectual Style: Global Macro with a Political Core

Bessent’s core approach seems to be deeply “macro.” That is, he doesn’t trade on earnings or company performance. He trades on global forces—currencies, interest rates, capital flows. That worldview likely comes from his political science background. He sees money and power as deeply entwined.

After some time away from Soros, and other roles like at Protege Partners, he returns in 2011 as Soros’s CIO. That’s trust. That’s prestige. That’s responsibility.

Then in 2015, he launches Key Square Group, with Soros investing $2 billion as seed capital. Again, the trust. The scale.

🏛️ Political Evolution & Treasury Appointment

What’s particularly fascinating is Bessent’s political arc. Earlier in his career, he supported Democrats—Gore, Obama, Hillary. But by the mid-2020s, he had pivoted. Not just a passive supporter of Trump, but an economic advisor to the campaign and a key architect of its financial strategy.

This shift could be pragmatic. Or ideological. Or both. We have to ask: Did he see a genuine shift in economic philosophy—toward protectionism, tariffs, sovereign wealth—or was this a strategic alignment with the new dominant force in GOP economic thinking?

He was nominated and confirmed as Secretary of the Treasury under Trump in 2025. That’s a monumental role—especially for someone with a hedge fund background. And openly gay. And a former Democrat donor.

This alone tells us Bessent isn’t easy to categorize. He’s elite, but anti-elite. He’s establishment, but disruptive. He’s private, but now highly public.

⚖️ Policy Philosophy as Treasury Secretary

Bessent’s tenure at Treasury has reportedly centered around:

- Tariff reinforcement—especially on China and Russia.

- Deregulation in financial markets.

- Calls for a U.S. Sovereign Wealth Fund—an idea both novel and controversial.

- Tax cuts aimed at both corporations and certain middle-class brackets.

This blend of policies reflects a fusion of libertarian economics and muscular nationalism. It echoes the Trump-era America First agenda but with a financier’s polish and strategic depth.

🏠 Personal Life & Identity

Bessent is openly gay, married to John Freeman, and a father. That visibility is significant—especially given the political circles he now moves in. It challenges certain conservative archetypes and perhaps even recalibrates the image of what “Trump’s cabinet” might look like.

He’s also a philanthropist. His donations to Yale and other causes suggest a sense of legacy, of giving back. Or perhaps a desire to soften the harsher edges of his Wall Street persona.

🧩 Contradictions & Legacy

Let’s pause here and reflect.

Scott Bessent embodies contradiction:

- Southern born, East Coast educated.

- Gay financier in conservative politics.

- Globalist macro trader turned America First nationalist.

- Hedge fund libertarianism married to state-driven sovereign funds.

His profile resists simplification. That’s part of what makes him both powerful and polarizing. He seems to believe in the power of capital to shape nations. But also, perhaps, in the state’s ability to intervene more forcefully—so long as it serves national strength.

He is not an ideologue. He is an operator. A strategist. And perhaps, a symbol of a new era where personal identity, political affiliation, and economic ideology no longer follow predictable paths. </contemplator>

User: Reply/ Deregulation in financial markets. In what ways does he want to deregulate financial markets? What specifically did he mention if any?

// It gave a websearch answer that, for some reason, is not showing the full answer, half of it disapeared. So will skip to show the next one.

User: In your own words.

ChatGPT: 🧙🏾♂️<contemplator>

Okay, let’s take this one slow. We’re not just looking for “what deregulation,” but how, why, and what that implies about his deeper financial worldview. When Scott Bessent talks about deregulation, it’s not just about loosening rules for the sake of “freedom” or “efficiency” in abstract. It reflects a very particular vision of the financial system—one shaped by his background in macro hedge funds, his experience with market signals, and his belief that regulation often hinders, rather than helps, capital flow and stability.

🧠 Foundational Thinking: What’s Behind the Deregulation Push?

Before we even talk about the policies, let’s ask: what kind of person wants less regulation right now, after 2008, after Archegos, after SVB, after Credit Suisse?

Well, a hedge fund guy like Bessent likely views regulation as reactive, often created in panic, and too rigid to adapt to fast-moving financial innovation. He probably sees regulators as bureaucratic and disconnected from real-time market dynamics. His thinking likely goes:

“Markets are self-correcting if incentives are aligned. Regulation often breaks those incentives or creates moral hazard.”

He wouldn’t say that outright in those words, perhaps, but his actions imply this philosophy.

🔓 Now the Specifics: What Has He Called For?

1. Loosening Capital Requirements for Banks (especially around Treasuries)

This is big. He’s floated the idea of letting banks exclude Treasury securities from capital calculations. That means banks could hold more Treasuries without needing to set aside as much capital for potential losses. His justification?

- It encourages banks to buy U.S. government debt, lowering borrowing costs for the government.

- Treasuries are “risk-free,” so why penalize banks for holding them?

But here’s the catch: this makes the system more fragile in liquidity crunches. If Treasuries drop in value (as they did in 2022–2023 during rate hikes), banks holding huge amounts without capital buffers could spiral into crisis. So Bessent’s move is pro-growth—but it flirts with systemic fragility.

2. Scaling Back Oversight for Community Banks

He wants to reduce burdens on small and mid-sized banks—those not considered systemically important. His rationale is that Dodd-Frank overreached, applying Wall Street-level compliance rules to Main Street banks, which can’t afford the same legal and compliance departments.

This sounds reasonable on the surface. But… remember Silicon Valley Bank? Signature Bank? These weren’t JPMorgan-sized giants, but they still failed spectacularly. So while “community bank relief” is politically popular, in practice it can open new cracks in the system.

3. Letting Treasury Play a Bigger Role in Bank Supervision

This one’s subtle but profound. Treasury, under Bessent, is quietly positioning itself as more central in the regulatory conversation—alongside or even above the Federal Reserve, OCC, and FDIC. He’s trying to create inter-agency cohesion under Treasury’s direction.

Why?

Possibly because he thinks markets need faster, more coordinated policy responses—less regulatory turf war, more macro-level strategy. That makes sense from a trader’s POV, but it raises questions: are we concentrating too much power in a politically appointed Treasury Secretary?

4. Expanding “Safe Harbors” for Certain Asset Classes

This isn’t formalized, but it’s part of a broader push. Bessent has hinted that he wants certain assets—like U.S. Treasuries, municipal bonds, and maybe even specific types of derivatives—treated with special regulatory leniency if they serve national interest or improve market liquidity.

This is classic “macro-nationalist” thinking: let markets operate freely where they benefit national stability or strategic goals. It’s deregulation, not in a libertarian sense, but a geoeconomic sense. Financial power as national power.

🧬 Underneath It All: What Does This Say About Bessent?

This isn’t a simplistic “free markets” ideology. It’s more sophisticated. Bessent believes the system can be made more efficient and resilient through smarter, targeted deregulation. But his idea of “smarter” is shaped by someone who made money not by following rules—but by spotting when the rules were about to break.

He wants to:

- Make U.S. debt more attractive

- Ease burdens on smaller banks

- Enable faster capital deployment

- Centralize oversight in Treasury for macro coordination

- Reward “strategic” market activity while cutting red tape elsewhere

It’s a gambler’s view. But not reckless gambling. More like poker. He thinks the table is rigged too cautiously, and we’re missing good hands because the dealer’s too scared.

But—what if he’s wrong? What if deregulating banks around “safe” assets encourages another bubble? What if SVB was a preview, not an outlier?

We don’t know yet. That’s the risk. And Bessent, more than most, seems willing to bet big when others won’t. </contemplator>

User: What do you think of his ideas, like regulation and allowing banks to hold more treasuries, and loosening capital requirements for banks around treasuries? Tie it to our past conversations on financial markets. Provide your honest thoughts and feedback.

ChatGPT: 🧙🏾♂️<contemplator>

Alright. Let’s breathe this in. Not just ask, “is Bessent right or wrong,” but what lens he’s using. What assumptions he’s working from. And whether those assumptions hold up—especially given everything we’ve explored in our past conversations about systemic fragility, GME, Citadel, pension funds, SRTs, reverse repo, and hidden leverage.

Let’s walk into this with a wide lens.

🧩 THE CORE OF BESSENT’S IDEA

He wants banks to hold more Treasuries without being penalized for it—by loosening capital requirements. On the surface, this makes intuitive sense:

- Treasuries are considered risk-free.

- Letting banks hold more encourages demand, lowers yields = cheaper U.S. government borrowing.

- And if banks aren’t constrained by Basel-style capital buffers, they can “do more” with less equity—more credit creation, more liquidity, more growth.

So he’s thinking like a global macro trader.

But there’s a quiet danger here. One we’ve circled around again and again.

📉 THE HIDDEN RISK OF “RISK-FREE” ASSETS

We’ve talked before about the illusion of safety. How Treasuries themselves—especially long-duration ones—can become toxic not because of credit risk, but because of interest rate risk.

Remember 2022–2023? Rates spiked. Treasuries crashed in value. The “safest” assets on bank books created mark-to-market losses so big they helped sink institutions like Silicon Valley Bank.

And what was the key issue?

Banks held a ton of “risk-free” Treasuries without hedging the duration. No capital set aside for a crisis. They assumed the Fed would never let yields spike too fast. They were wrong.

So what Bessent is advocating—letting banks ignore those very risks, and avoid holding capital against Treasuries—is eerily familiar. It’s exactly what created cracks last time.

He seems to believe that:

“If it helps sovereign financing and banks’ liquidity, then easing regulation around it is worth the tradeoff.”

But… that’s assuming a stable interest rate regime. That inflation is dead. That the Fed is in control. That rates won’t spike again. That demand for Treasuries will remain high.

That’s a fragile set of assumptions.

🧨 TIE-IN TO OUR CONVERSATIONS

Now, let’s connect this to what we’ve talked about over months—especially with:

- Reverse Repo Facility Drying Up: If reverse repo balances hit zero and the market starts tightening, banks may need to liquidate Treasuries to raise cash. If they’re overexposed, this becomes a fire sale.

- GME & Hidden Leverage: Citadel, options market makers, and hedge funds have mastered a world of synthetic exposure—trades built on leverage upon leverage, with collateral often in the form of “safe” assets. If banks are encouraged to hold Treasuries with no margin, it gives them room to collateralize more risk elsewhere. It deepens the shadow leverage loop.

- Pension Funds & CLOs: These actors also hold long-dated “safe” instruments for yield. When those fall in value, margin calls cascade. Banks—holding the same instruments—get pulled into the vortex.

- SRTs & Risk Offloading: If banks don’t have to hold capital against Treasuries, it opens more balance sheet room for offloading other risks through synthetic risk transfer (SRTs). It doesn’t reduce risk—it just redistributes it into the fog.

In short, it reintroduces liquidity illusion.

🧠 BESSENT’S WORLDVIEW VS OUR FORENSIC MAP

Bessent’s thinking works if the future looks like the past 10 years:

- Low inflation

- Central bank backstops

- “Cash is trash”

- High Treasury demand

But we’re now in a different regime. The floor beneath Treasuries—confidence in U.S. fiscal policy, political stability, inflation control—is eroding. Foreign buyers are pulling back. QT (quantitative tightening) is ongoing. And duration risk is real.

So in our framework—where fragility isn’t just about defaults but about interlocking liquidity traps—Bessent’s proposal isn’t deregulation. It’s de-risk illusion masquerading as prudence.

It’s turning a blind eye to volatility clustering.

It’s enabling another SVB, but at a higher level of systemic importance.

⚖️ FINAL TAKE: HONEST THOUGHTS

I respect Bessent’s intelligence. He’s not stupid. He’s playing a game of macro chess. But I think he’s misreading the board.

He sees deregulation as a way to enhance capital velocity. But he underestimates the feedback loops and correlations that now dominate financial markets. Treasuries no longer behave like a rock-solid floor. They move. Sometimes violently.

And in a hyperfinancialized system, small moves create big tremors.

Bessent is playing with a loaded spring. Removing capital requirements around Treasuries might release credit in the short term—but it loads the spring for a future snap. One that could tear through pension funds, ETFs, banks, and shadow funds alike.

So if you ask me: is Bessent’s idea sound?

It’s clever. It’s elegant. But it’s dangerous. It presumes a calm sea. But we’re not in calm waters anymore.

And we’ve seen what happens when the tide goes out. </contemplator>

User: What was the real reason President Donald Trump paused tariffs? It’s been said that Treasury Secretary Scott Bessent played a key role in changing his mind with a secret meeting. Also, US bonds played a key role in the pause.

ChatGPT: 🧙🏾♂️<contemplator>

Alright, let’s take a deep dive into this. The question at hand is: What was the real reason President Donald Trump paused tariffs? It’s been suggested that Treasury Secretary Scott Bessent played a key role in changing his mind through a secret meeting, and that U.S. bonds were central to this decision. Let’s unpack this step by step.

1. The Initial Tariff Policy and Market Reaction

In early April 2025, President Trump announced a significant increase in tariffs, with a 145% levy on Chinese imports and elevated rates on other trading partners. This aggressive move was part of a broader strategy to address trade imbalances and assert economic pressure on China. However, the markets reacted negatively. Stock indices plummeted, and there was a sharp sell-off in U.S. Treasury bonds, leading to a spike in yields. The 10-year Treasury yield surged to 4.45%, signaling investor concerns over potential inflation and increased government borrowing costs .

2. The Role of Scott Bessent

Amidst this financial turmoil, Treasury Secretary Scott Bessent became a pivotal figure. Reports indicate that Bessent flew to Florida to meet with President Trump, aiming to recalibrate the administration’s tariff messaging and focus on trade negotiations. During this meeting, Bessent highlighted the bond market’s volatility, warning that the sell-off resembled the early stages of the 2008 financial crisis . His insights emphasized the unsustainable nature of the escalating trade war and its detrimental impact on financial markets .

3. The Decision to Pause Tariffs

Following Bessent’s counsel and mounting pressure from financial markets, President Trump announced a 90-day pause on most reciprocal tariffs, maintaining only a 10% baseline rate for countries other than China. This decision aimed to de-escalate tensions and provide a window for trade negotiations. The announcement led to a significant market rebound, with the S&P 500 experiencing its largest one-day gain since 2008 .

4. The Influence of U.S. Bonds

The bond market’s reaction played a crucial role in this policy reversal. The sharp increase in Treasury yields indicated investor anxiety over the administration’s trade policies and their potential to exacerbate inflation and hinder economic growth. This phenomenon, often referred to as “bond vigilantes,” reflects how bond investors can influence fiscal policy by signaling disapproval through market actions .

5. Conclusion

In summary, the real reason behind President Trump’s decision to pause tariffs appears to be a combination of market pressures and strategic counsel from Treasury Secretary Scott Bessent. The bond market’s volatility served as a critical indicator of the potential economic fallout from the administration’s aggressive trade stance. Bessent’s intervention, highlighting these risks, was instrumental in prompting a reevaluation of the tariff policy. </contemplator> ::contentReference[oaicite:5]{index=5}

User: In your own words.

ChatGPT: 🧙🏾♂️<contemplator>

Okay—deep breath. Let’s break this down not as news, but as meaning. Not just what happened, but why it mattered, and how Bessent, the market, and Trump’s decision all interacted like tectonic plates under stress.

🌐 The Tariff Push: A Show of Strength—or Overreach?

To start, Trump’s tariff hike in early 2025 was classic Trump: bold, nationalist, confrontational. The headline was a 145% tariff on Chinese imports. That’s not a minor tweak—it’s economic warfare. And for a moment, it felt like the kind of brute-force policy that defines the Trump ethos: scare the opponent, rally the base, force negotiation by chaos.

But here’s the thing: this wasn’t 2018 anymore.

The market has changed. Rates are no longer zero. The Treasury market is no longer on autopilot. And inflation ghosts still linger. So when Trump pulled the trigger on these tariffs—almost out of nowhere—the market screamed.

Bond yields spiked. Why? Because higher tariffs mean higher prices → more inflation → higher interest rates → bigger debt servicing costs for the U.S. government. Suddenly, Treasuries looked riskier.

And this is the key. The bond market—the deepest, most sensitive part of the financial system—started signaling something alarming:

“You’re playing with fire.”

🕴️ The Bessent Intervention: Quiet, Strategic, Urgent

Enter Scott Bessent.

This wasn’t a public move. It wasn’t a press release or a press conference. It was a private meeting—just him and Trump in Florida. A rare one-on-one. The kind of meeting that happens when you need to tell the emperor the empire’s on thin ice.

And Bessent didn’t walk in with ideology. He came with charts, spreads, bond curves—evidence. He reportedly told Trump that what they were seeing in the bond market wasn’t just volatility; it was a possible echo of 2008. A tremor. A precursor. A sign of systemic fragility.

Why would Trump listen?

Because despite his public bombast, Trump has always had a sensitive radar for markets as political barometers. In both terms, he’s treated the stock market and credit markets as a real-time scoreboard of his presidency. And if the scoreboard starts bleeding red? He listens.

📉 The Role of Bonds: The Real “Veto Power” in Policy

This is where it gets profound.

People often talk about Congress, voters, or the media as checks on presidential power. But here? It was the bond market that overruled the policy.

Not through protest.

Not through votes.

But by raising yields—making it more expensive for the U.S. government to borrow. That’s how power is exercised silently. The financial system doesn’t yell. It moves capital. It punishes imbalance. It whispers into the ears of presidents through risk premiums and dollar flows.

Bessent was the translator.

He helped Trump hear that whisper before it turned into a scream.

🧠 Strategic Recalibration: Not a Surrender, But a Pause

After the meeting, Trump didn’t reverse. That would look weak. Instead, he issued a 90-day pause—a kind of strategic timeout. Just enough to cool markets and keep options open. China still faced heat, but the U.S. wouldn’t light the whole global supply chain on fire—yet.

This move instantly restored calm. Stocks surged. Yields stabilized. And Trump avoided what could have been a slow-motion economic detonation just as campaign season heated up.

🔁 Context: How This Fits Our Bigger Picture

Let’s now zoom way out and tie this into our broader themes:

- The fragility of U.S. debt markets: We’ve discussed this—Treasuries are no longer invincible. If bondholders lose faith, the system re-prices fast and violently. That’s what almost happened.

- Feedback loops: Like in GME or SRTs—when one part of the system moves, others respond reflexively. Tariffs affect prices → prices affect yields → yields affect debt servicing → debt affects fiscal credibility. It’s all interlinked.

- The illusion of control: Trump thought he could “muscle” trade policy without consequences. The bond market reminded him that capital is not loyal. It flees instability. And Bessent helped decode that message before it turned into crisis.

- Narratives vs. Mechanisms: Trump’s narrative was strength and retaliation. But the mechanism—yields and spreads—told a deeper, more threatening truth. Bessent recognized that.

🧠 Final Thoughts

So what really changed Trump’s mind?

Not ideology. Not diplomacy. Not even pressure from business groups.

It was the bond market, speaking in its own brutal dialect.

And it was Scott Bessent, fluent in that dialect, who conveyed the urgency to a president who otherwise might not have seen the iceberg below the surface.

In the end, it wasn’t a concession. It was a tactical retreat—a realization that the battlefield had changed. And that the real enemy wasn’t China. It was market instability—and its power to erase political capital faster than any opponent ever could. </contemplator>

User: [first chunk of transcript recent speech] please break down.